{kind=link}

Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

Plugin vehicles are all the rage in the Chinese auto market, even in the slowest month of the year — due to the Chinese New Year celebrations. Due to the fact that festivities occurred this year in February, and last year they were in January, the market had an apparently so so month, with plugins scoring 440,000 sales (in a 1.33-million-unit overall market). That’s down 9% year over year (YoY).

But considering that this February had fewer work days than in the previous year, due to the New Year festivities, then even a single-digit drop is a positive sign. Looking deeper at the numbers, BEVs were down 22%, while PHEVs still managed to grow 22% in February! That’s an amazing performance for the technology, which is currently experiencing a golden age in the Chinese market.

This pulls the year-to-date (YTD) tally to close to 1.1 million units, and with March set to be another strong month, we should see Q1 end on a positive note.

Share-wise, February saw plugin vehicles hit 33% market share! Full electrics (BEVs) alone accounted for 22% of the country’s auto sales. This pulled the 2024 share also to 33% (20% BEV), and considering that the last month of the quarter is usually a strong month, we can assume that the country’s plugin vehicle market share will end around the 35% mark in Q1, and the first half of the year should see it already close to 40%.

{kind=link}

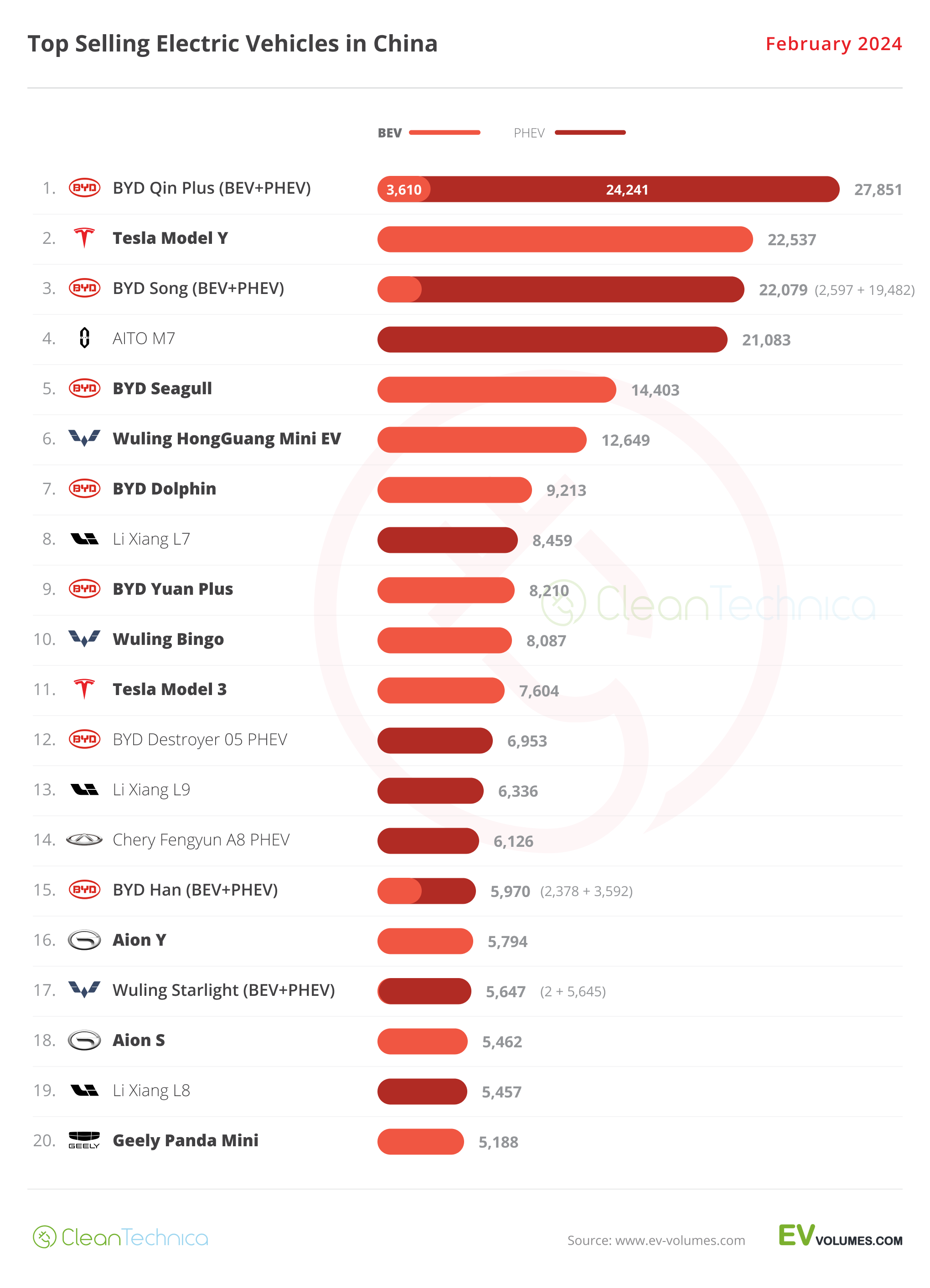

Regarding last month’s best sellers table, the top 4 best selling models in the overall table exactly mirrored the ones in the EV table. Which once again proves the merging process that we are witnessing between the two tables. Here’s more info and commentary on February’s top selling electric models:

#1 — BYD Qin Plus (BEV+PHEV)

Along with the Song, the BYD Qin has been a bread and butter model for the Chinese automaker for a long time. The midsizer reached 27,851 registrations in February. This allowed it to be the best seller in the overall market, and with the sedan being the first pawn launched by BYD in its recent “War on ICE” campaign (aka price cuts), expect it to be the first model to benefit from the sales pickup, probably already in March. With the recent price drop and prices now starting at 80,000 CNY ($12,000), demand is bound to spike again. Despite the strong internal competition — a new, fancier Qin L is said to be launching soon, expect BYD’s lower priced midsize sedan to continue posting strong results at the cost of the competition, EV or ICE, all while keeping its most direct competitors — the Tesla Model 3, Wuling Starlight, and GAC Aion S — at a safe distance.

#2 — Tesla Model Y

Tesla’s star model got 22,537 registrations, which allowed it to land in 2nd in the overall ranking. It seems the US crossover has found its cruising speed in the Chinese market, at around 25,000–30,000 units a month. While that doesn’t make it the best seller in the market, it allows it and the Model 3 to be the only two foreign EVs to run at the same pace as the domestic brands (Volkswagen, take notice).

#3 — BYD Song (BEV+PHEV)

BYD’s midsize SUV is the uncontested leader in the Chinese automotive market, but this time, the star player had to concede the leadership position to its Qin Plus sibling(s), scoring “just” 22,079 registrations. Will the Song continue to rule in the Chinese automotive market? Well, it depends on the competition, especially the internal competition. Currently, the Song only has the recently introduced Song L as internal competition, but the upcoming Sea Lion and the premium car-on-stilts Denza N7 (a car that sits somewhere between the Tesla Model Y and the Zeekr 001) are both also wanting a piece of the pie. This is probably too much competition inside BYD’s midsize SUV portfolio for the Song to continue clocking 40,000–50,000 sales/month, a necessary threshold to continue leading the cutthroat Chinese auto market.

#4 — AITO M7

After a shot in the arm by Huawei in the second half of last year — a refresh and lower prices — the joint venture brand between Seres Group and Huawei has found its mojo. The full size SUV became an instant success. While its first surging sales months last year might have raised some eyebrows and raised the question of whether the joint venture could replicate Li Auto’s successful formula (5-meter EREV SUVs with 40 kWh-ish batteries), it seems not only can they replicate the startup’s success, but they can bring a market disruptor to the field and revolutionize the full size category! I mean, a full size SUV ending in the overall top 5? Wooooow. … Expect the competition to launch copycats large EREV SUVs soon. In February, the AITO model hit 21,083 registrations.

#5 — BYD Seagull

Things continue to go well for the hatchback model, with the small EV securing another top 5 presence thanks to 14,403 registrations. With part of production now being diverted to export markets, it seems demand for the little Lambo is now at cruising speed in China. The perky EV is now in top 5 territory. Even with its attention now diverted to other geographies, like Latin America and Asia-Pacific, expect the little BYD to continue being part of the BYD pack that populates the Chinese top 10. What about export prospects to Europe? There are talks that the model will be launched in Europe in the second half of the year. Of course, do not expect the low prices in Europe that the Seagull has in China. When the city EV lands, as the Dolphin Mini, European prices will be significantly higher for a number of reasons (tariffs, VAT, etc.), but I wouldn’t be surprised if it started to be sold here at 17,999€ … which would still be a killer price considering the direct competition is still north of 20,000€.

Looking at the rest of the best seller table, the highlight comes from Wuling, which placed three models in the table. The bare basics Mini EV was in 6th, the supermini Bingo was in 10th, and the new Starlight sedan was in 17th. The SAIC–GM brand lineup is starting to look quite complete. Now they only need a compact best seller, a sort of … Bingo Plus?

The sportier sibling of the BYD Qin Plus, the Destroyer 05, also had a great month, with 6,953 registrations, allowing it to end the month in 12th. That’s just below the category runner-up, the #11 Tesla Model 3. Does this mean the Qin in sportier frock will become a regular face in the table throughout the rest of the year? To be continued….

But the biggest surprise in the table is in 14th, the Chery Fengyun A8 PHEV, a sedan destined to compete against the BYD Qin-family. With roughly the same size as the BYD sedan but higher starting prices (120,000 yuan vs 80,000 yuan), and similar EV specs (18kWh battery), it will be interesting to see how well the new Chery will do in a segment (sedans) where the brand does not have strong traditions. But with 6,126 units in only its 2nd month on the market, it has gotten off to a good start….

Outside the top 20, there was another recent model shining, with the Cadillac Escalade sized AITO M9 registering 5,251 units in February, its 3rd month on the market. Will AITO’s new flagship yacht be as successful in its category as the M7? Currently, the leader in the humongous SUV category is the Li Xiang L9 (13th in February, 6,336 sales). So, the distance isn’t that big….

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

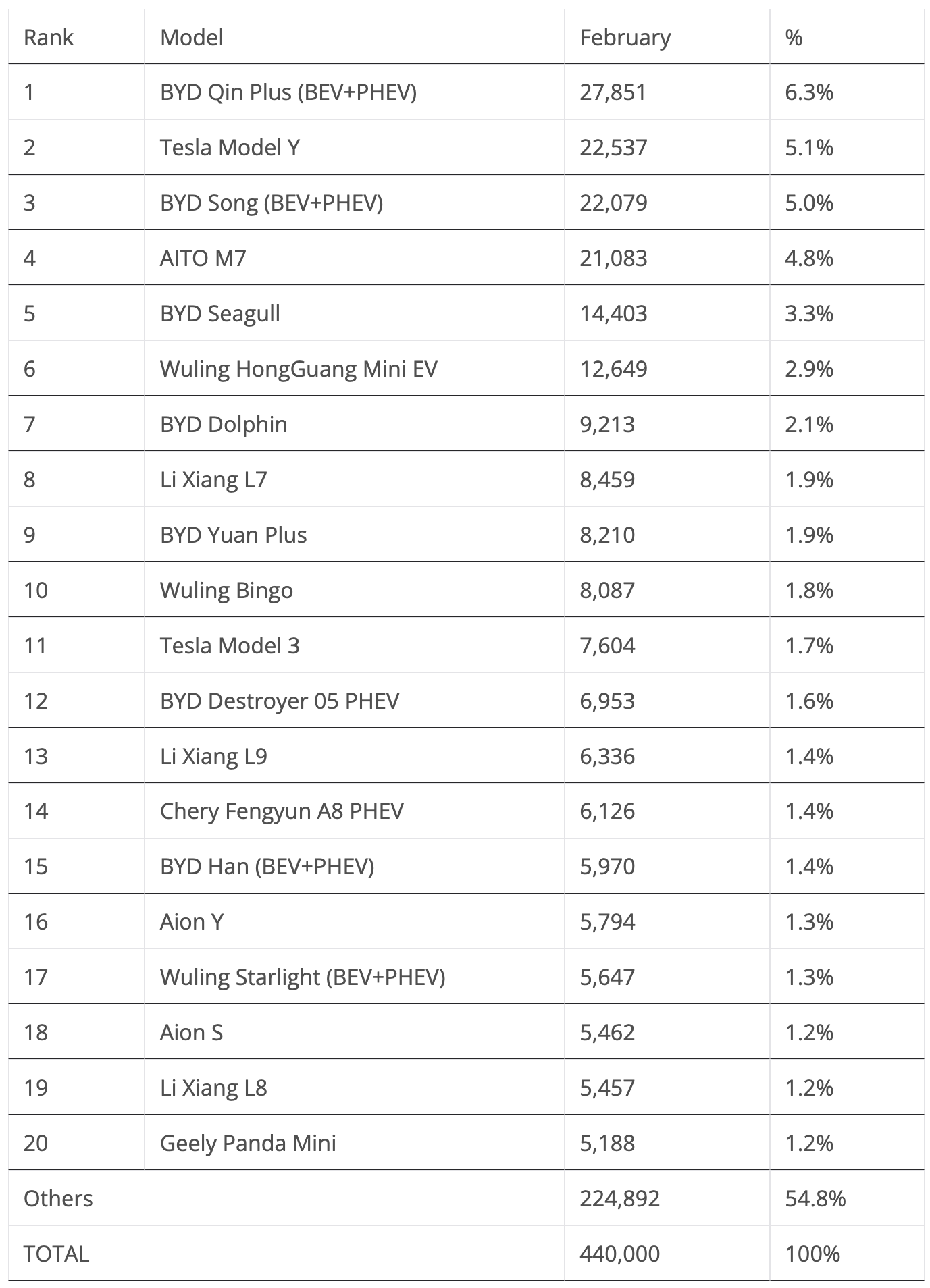

The 20 Best Selling Electric Vehicles in China — January–February 2024

Looking at the 2024 ranking, the leading BYD Song is well above the competition, but below it, there is a lot to talk about.

The BYD Qin Plus switched positions with the AITO M7, with the BYD sedan jumping into the runner-up position, while the Huawei-backed SUV dropped to 4th.

The Wuling Mini EV was up to 6th, while the Li Xiang L7 climbed one position, to 9th.

In the second half of the table, the highlights are the Tesla Model 3 jumping three positions, to 12th, while the flagship Li Xiang, the L9, was up to 17th.

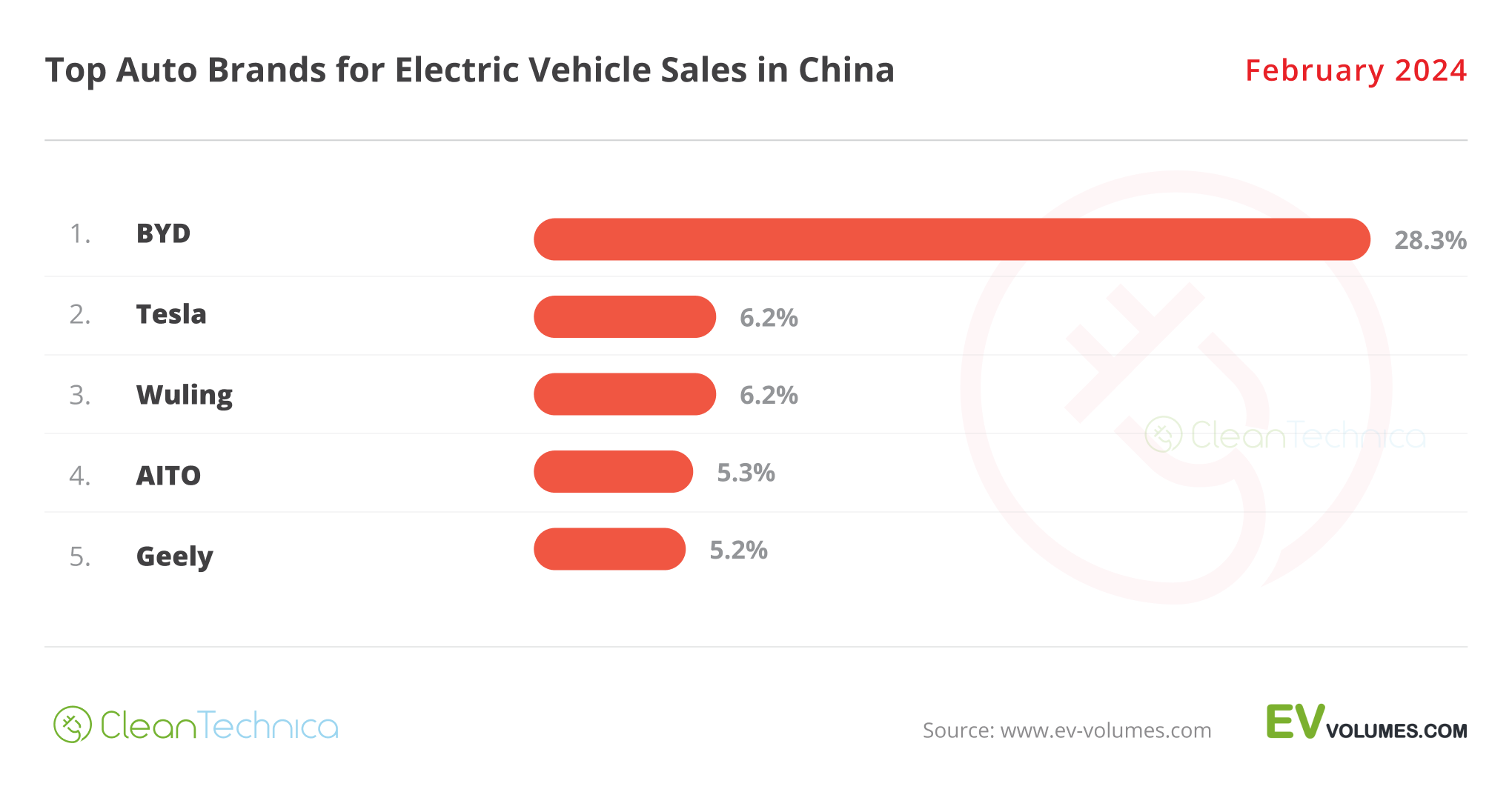

Auto Brands Selling the Most Electric Vehicles in China

Looking at the auto brand ranking, there’s some major news, but not at the top. BYD (28.3%, down from 28.5%) remains as stable in its leadership position as ever.

Things get more interesting below, though. Tesla (6.2%) and Wuling (6.2%) are battling it out for the #2 spot, while Geely suffered from a slow month in February (best seller Panda Mini was only 20th) and dropped from #2 to #5.

AITO (5.3%) also had a good month, jumping to 4th and kicking out Li Auto from the top 5! So, the Huawei-backed startup is now the hottest startup in town! If AITO can replicate the M7 success with the recently introduced M9, then the runner-up position could be a possibility for the brand….

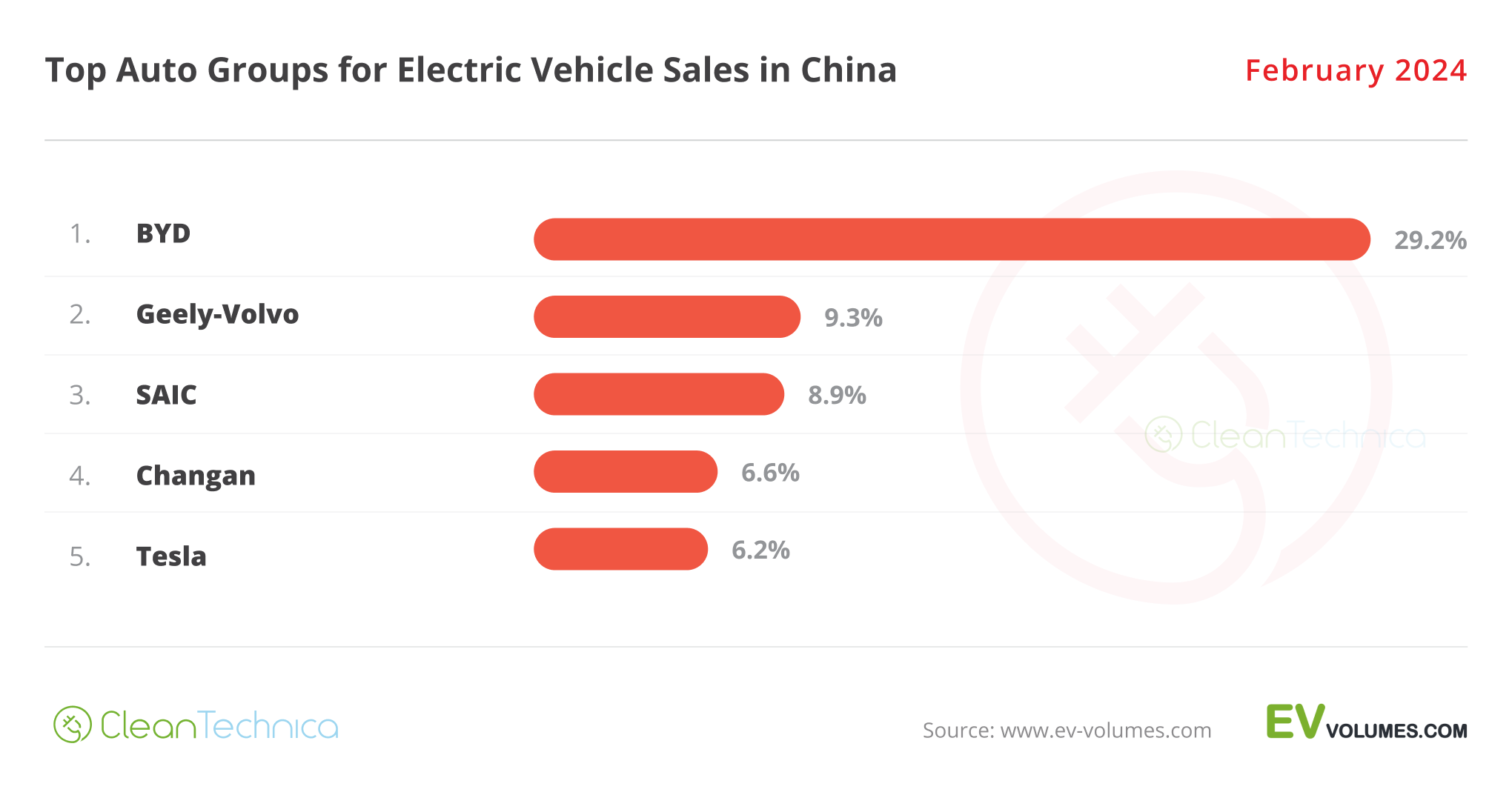

Auto Groups Selling the Most Electric Vehicles in China

Looking at OEMs/automotive groups/alliances, BYD is comfortably leading, with 29.2% share of the market, while Geely–Volvo is a distant runner-up, with 9.3% share, and is being threatened by a rising SAIC (8.9%), now in 3rd (benefitting from the good moment of its Wuling brand).

Changan had a slow month and dropped to 4th, with 6.6% share. The OEM was unable to place any model in the February top 20.

Tesla (6.2%, up from 6%) is in 5th, and the US make expects to stay among the top 5 during the rest of the year. Though, given market dynamics and Tesla’s lack of fresh metal, it will be a hard task to fulfill.

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Latest CleanTechnica.TV Video

CleanTechnica uses affiliate links. See our policy here.